Understanding Your Credit Score

Banks, credit card companies and other businesses use credit scores to estimate how likely you are to pay back money you borrow. Here’s what you should know.

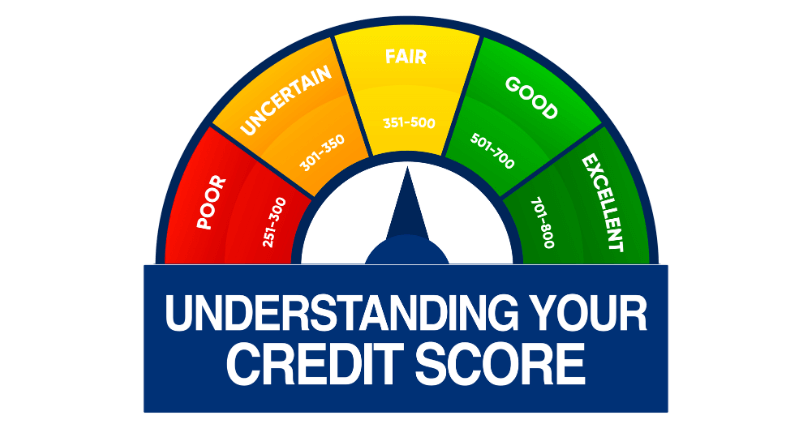

A higher score makes it easier to qualify for a loan and lower interest rates. Many scores range from 300 to 850, but know that different companies use different ranges. Here’s what else you should know.

YOU HAVE MANY CREDIT SCORES

You can have more than one score, because:

- Lenders use different scores for different products

- There are many different credit scoring formulas

- Information can come from different credit reporting sources

For example, a credit card score could be different from a home loan score, and any scores you purchase online could be different from both of those. For some people, these differences aren’t that big. But because lenders use different scores, you might qualify for lower rates with one lender and not another. It can pay to shop around.

WHERE DO CREDIT SCORES COME FROM?

Where do credit scores come from? Your credit scores are generally based on information in your credit reports. This information is reported by your lenders to credit reporting companies. The three biggest are Equifax, Experian, and TransUnion.

Several variables affect your credit score, including:

- How many credit accounts you have

- How long you’ve had those accounts

- How close you are to your credit limit

- How often your payments have been late

- Other factors

HOW TO RAISE YOUR CREDIT SCORE

- Paying your bills on time, every time, has the greatest impact on your score.

One way to make sure your payments are on time is to set up automatic payments or set up electronic reminders. If you have missed payments, get current and stay current.

- Don’t get close to your credit limit.

Credit scoring models look at how close you are to being “maxed out,” so try to keep your balances low in proportion to your overall credit limit. Experts advise keeping your use of credit at no more than 30 percent of your total credit limit.

- A long credit history helps your score.

Credit scores are based on experience over time. Your score improves the longer you have credit, open different types of accounts, and pay back what you owe on time.

- Be careful closing accounts.

If you close some credit card accounts and put most or all of your credit card balances onto one card, it may hurt your credit score if you are using a high percentage of your total credit limit. Frequently opening accounts and transferring balances can hurt your score too.

- Only apply for credit you need.

Credit scores take into account your recent credit activity as an indicator of your need for credit. If you apply for a lot of credit over a short period of time, it may appear that your money situation has changed for the worse.

Find a Mortgage Lender

Start your search for mortgage lenders

YOUR CREDIT REPORT MATTERS AS MUCH AS YOUR CREDIT SCORE

Mistakes in your credit reports could hurt your credit history and credit score, so check them regularly. You can get one free credit report from each of the big three credit reporting companies every 12 months. Go to www.annualcreditreport.com or call 877-322-8228. In addition, Equifax offers six free credit reports every 12 months until December 31, 2026. When you visit the site, you may see steps to view more frequently updated reports online. This gives you a greater ability to monitor changes in your credit.

WHAT TO LOOK FOR WHEN YOU GET YOUR CREDIT REPORT

- Mistakes in your name, phone number, or address

- Loans, credit cards, or other accounts that are not yours

- Reports saying you paid late when you paid on time

- Accounts you closed that are listed as open

- The same item showing up more than once (like an unpaid debt)

HOW TO FIX MISTAKES

If you find something wrong in your credit report, you may contact both the credit reporting company and the company that provided the information (for example, your credit card company). Explain what you think is wrong and why. Include copies of documents that support your dispute. Your credit reports come with instructions on how to dispute mistakes.

SOURCE: The Consumer Financial Protection Bureau regulates the offering and provision of consumer financial products and services under the federal consumer financial laws, and educates and empowers consumers to make better informed financial decisions. Learn more at www.consumerfinance.gov

Get answers to money questions at www.consumerfinance.gov/askcfpb

New Homes Guide Magazine

The latest new home trends, up-and-coming neighborhoods, and more.

© RGV New Homes Guide, 2024. Unauthorized use and/or duplication of this material without express and written permission from this site’s author and/or owner is strictly prohibited. Excerpts and links may be used, provided that full and clear credit is given to RGV New Homes Guide with appropriate and specific direction to the original content.